SK Innovation E&S (hereafter SKI E&S), the division responsible for SK Innovation’s Liquefied Natural Gas (LNG) and eco-friendly energy businesses, is gaining attention in the market for its efforts to expand the LNG value chain and enhance cost competitiveness. Leading domestic and international financial institutions, including SK Securities, Hyundai Motor Securities, and CGS International (CGSI), have recently published reports analyzing how SKI E&S’s LNG value chain expansion could positively impact SK Innovation’s corporate value, prompting upward revisions to their target stock prices.”

| “SKI E&S: Securing Dominant Competitiveness Through an Integrated LNG Value Chain”

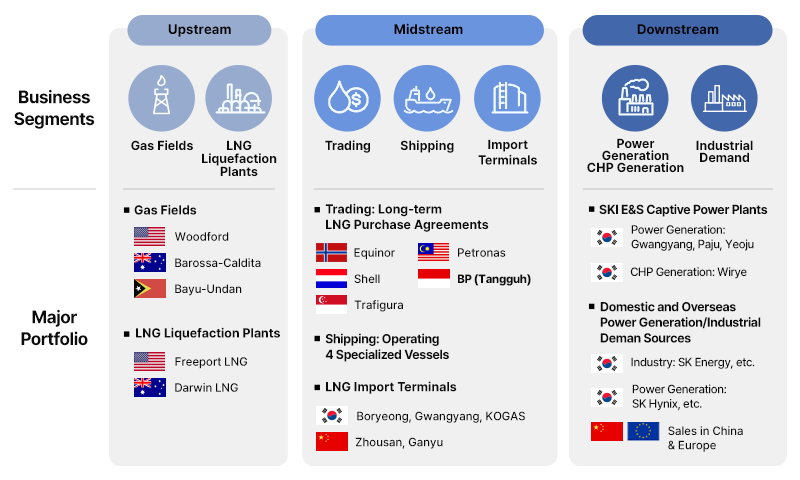

SK Securities has analyzed that SKI E&S has established unmatched business competitiveness through its integrated LNG value chain, spanning upstream (gas fields), midstream (transportation and terminals), and downstream (power plants). In particular, it was noted that SKI E&S is securing cost-competitive LNG through the liquefaction facility usage contract at the Freeport Terminal in the U.S. and various long-term purchase agreements, including those with the Tangguh gas field in Indonesia. To ensure stable adoption of these long-term contract volumes, securing downstream demand is crucial—a role fulfilled by SKI E&S’s LNG power plants located in Gwangyang, Paju, Yeoju, and Wirye in South Korea, with a combined capacity of approximately 4.4GW.

* SKI E&S’s Future plans include securing stable demand sources in locations such as Yongin (Semiconductor Cluster) and Wangsuk, also in South Korea.

Additionally, SK Securities highlighted how SKI E&S’s proprietary terminals, such as the Boryeong LNG Import Terminal, contribute to stable inventory management, which serve as positive factors in reducing procurement costs.1

| Enhancing Cost Competitiveness with the Barossa Gas Field Project

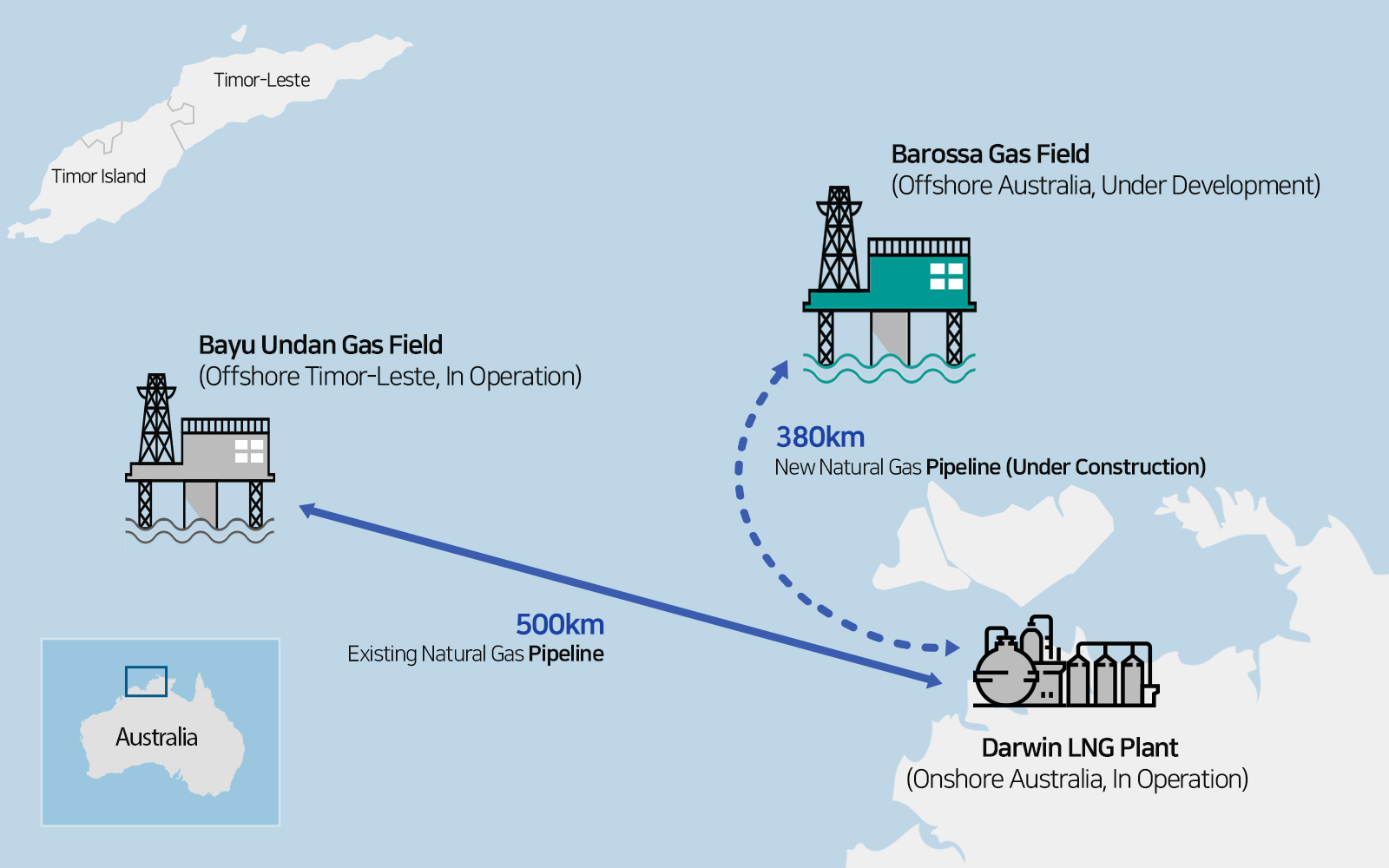

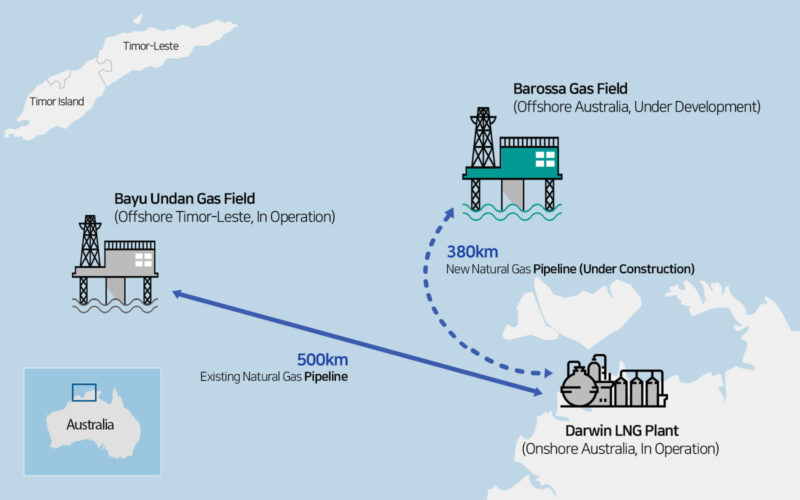

Starting in the second half of 2025, SKI E&S is set to produce 1.3 million tons of LNG annually from the Barossa gas field in Australia. Analysts at Hyundai Motor Securities forecast that the relatively low construction costs of the facilities involved in the Barossa Gas Field project will significantly bolster cost competitiveness.2

The Darwin LNG Plant, where natural gas from the Barossa Gas Field will be liquefied, stored, and shipped, is a Brownfield project* that leverages existing facilities. This approach enables considerable investment savings, with CAPEX (capital expenditure) estimated to be 20–25% lower compared to other projects.

** The Darwin LNG plant, which previously processed gas from the Bayu-Undan gas field, will now be repurposed to process gas produced from the Barossa gas field.

Additionally, SK Securities highlighted the logistical advantage of LNG produced at the Barossa Gas Field, with a transport time of just 8 days to South Korea. This is notably shorter compared to 25 days from the U.S. or 18 days from Qatar, resulting in substantial savings in transportation costs.3

CGSI also expects the operation of the Barossa gas field to significantly reduce SKI E&S’s gas procurement costs. As a result, CGSI has raised its target stock price for SK Innovation from KRW 135,000 to KRW 165,000. The firm also highlighted SKI E&S’s plans to expand its LNG trading volume from 5.3 million tons in 2024 to 10 million tons by 2030, projecting that this growth trajectory will have a positive impact on SK Innovation’s corporate value.4

▲ Panoramic view of the Barossa gas field in Australia

| “Recent Trends in the Global Energy Market Present New Opportunities for SKI E&S”

In addition, predictions that the easing of regulations on traditional energy sources, such as oil and gas, could create growth opportunities for SKI E&S have garnered attention. SK Securities forecast that the expansion of natural gas production and exports in the U.S. is likely to stabilize global LNG prices at lower levels. The firm also predicted that these changes in the global market would be key factors in strengthening SKI E&S’s competitiveness in the LNG value chain.5

| “LNG Business: Driving SK Innovation’s Future Growth”

LNG is increasingly recognized as a key energy source in the era of energy transition, offering both sustainability and economic feasibility. With SKI E&S securing strong cost competitiveness through its integrated LNG value chain, analysts expect the company to generate solid profits in its LNG power generation and trading businesses. In particular, the full-scale operation of the Barossa gas field and stable volume procurement are projected to further enhance SKI E&S’s profitability over time. This competitive edge in the LNG business is anticipated to contribute to SK Innovation’s overall earnings growth, delivering long-term and stable value to its shareholders.

Citations:

1. SK Securities Report, “SKI E&S Site Tour Review: Dominant LNG Value Chain Competitiveness”, February 25, 2025, p.6.

2. Hyundai Motor Securities Report, “U.S. LNG is Coming [Refining & Petrochemicals],” March 6, 2025, p.44.

3. SK Securities Report, “SKI E&S Site Tour Review: Unmatched LNG Value Chain Competitiveness,” February 25, 2025, p.4.

4. CGSI Report, “Unlocking LNG Value in 2025F”, February 27, 2025, p.1.

5. SK Securities Report, “SKI E&S Site Tour Review: Dominant LNG Value Chain Competitiveness”, February 25, 2025, p.14.