Geopolitics and Global Economics: Constraints on Energy Transition

Decarbonization is, at its core, a matter of economics. The global push to reduce carbon emissions is often attributed to a desire to contribute to the greater good, but in reality, national self-interest is a greater motivating factor. For Western economies, including the United States and Europe, the transition to carbon neutrality has offered tangible economic benefits — most notably by helping to curb inflationary pressures and strengthen energy security. Naturally, renewable energy aligns with these objectives due to its relatively low generation costs and reliance on domestically built infrastructure. Because of this, along with the fact that decarbonization is rooted in self-interest, the energy transition itself is structural.

While the energy transition is structural in nature, the pace is determined by the scale of the economic benefits it delivers — chiefly, price stability and energy security. The unprecedented zero-interest-rate environment that began with the 2008 global financial crisis and extended through the early 2020s — including the pandemic period — significantly improved the investment economics of climate-related projects and accelerated the energy transition. However, more recently, the landscape has shifted significantly. Massive fiscal stimulus packages and high-profile conflicts have triggered sharp inflation and rapid interest rate hikes. These events have profoundly altered the equation, leading to sharp increases in capital costs associated with renewable energy and the levelized cost of energy (LCOE). At the same time, returns on investments related to electric vehicles and batteries have deteriorated. As a result of a high-interest-rate environment such as this, the first core justification of the clean energy narrative — that the transition would help reduce price uncertainty — has become significantly weaker. In some cases, despite efforts to reduce costs, the shift to cleaner energy has instead contributed to higher costs. When this paradoxical dynamic occurs, it serves as a contributing factor to slowing the pace of the energy transition.

Securing energy independence by reducing fossil fuel reliance is the second frequently-cited justification for the energy transition, yet it faces a similar contradiction—one rooted in global supply chains. Batteries, the foundational asset of the renewable energy and electric vehicle era — as well as the minerals that account for roughly 50%of battery production costs — remain areas in which China holds overwhelming supply chain dominance. From the perspective of the United States and Europe, these circumstances mean a rapid energy transition would risk increasing dependence on China for critical energy. In this sense, a transition aimed at strengthening energy security could have the unintended effect of introducing new dependencies that are not desired.

These factors have converged to shape recent political outcomes. In both the 2024 U.S. presidential election and the European Parliament elections, political forces emphasizing a recalibration of climate and energy policies — often described as a “green backlash,” or growing public resistance to aggressive environmental agendas — gained traction. As a result, policy support for renewable energy and electric vehicles has been scaled back in several regions. While specific political events served as immediate triggers, the more important drivers lie beneath the surface. At the core of these shifts is an economic reality. Unlike the mid-2010s, when low inflation and a low-interest-rate environment pushed real risk-free rates into negative territory, the mid-2020s are defined by persistently high inflation and elevated interest rates. In this environment, everyday economic pressures related to cost of living have taken on greater urgency. Against this backdrop, a change to the speed of the energy transition is not simply a policy choice, but an increasingly unavoidable outcome.

A New Growth Narrative for the Battery Industry

As the world enters the mid-2020s, the battery industry is increasingly positioned not only within the framework of decarbonization, but also within the logic of geopolitical competition and national security. Unlike the decarbonization-driven market, where policy support and demand can fluctuate significantly with economic conditions, geopolitical trends and the pursuit of national security tend to function as more stable, long-term forces. From this perspective, the battery industry is approaching a critical inflection point. This new phase begins with the evolving dynamics between the United States and China.

As geopolitics shift, assets with security significance take on greater importance. Security assets can be defined as those whose control helps secure a country’s position as a leading power. Materials essential to sustaining everyday economic activity and conducting warfare — such as steel and energy resources including coal and oil — serve as representative examples. As a result of the increased focus on security assets, capital flows have also begun to flow toward them more. In October 2025, JPMorgan announced plans to invest USD 1.5 trillion over the next decade in industries linked to U.S. national security, citing areas such as energy storage systems and critical mineral supply chains. The Trump administration likewise undertook direct equity investments in private companies across several strategic sectors in the second half of 2025, including rare earths (July 2025), semiconductors (August 2025), minerals (September 2025), and quantum technologies (October 2025), describing these moves as investments aimed at safeguarding national security. Taken together, this large-scale flow of public and private capital ultimately points toward a single focal area: data.

In the twentieth century, oil and steel were treated as core security assets essential to sustaining everyday life and defense operations. Today, data serves the same purpose — but to a greater extent. To support higher standards of daily life and more advanced forms of defense, data has become indispensable. Palantir, founded with the mission of supporting U.S. national security, has come to symbolize the treatment of data as a security asset. As data has taken on this role, the strategies of global powers have increasingly been reframed as a prioritization of the development and control of data centers. Describing the race for artificial intelligence as a matter of defense is not merely rhetorical. In the second half of the twentieth century, the strategies of the United States and the Soviet Union focused on the accumulation of nuclear weapons. In the current era, strategies revolve around the race to secure AI data center capacity. The Stargate Project — an initiative announced by the U.S. government, OpenAI, Oracle, and SoftBank involving planned investments in AI infrastructure of up to USD 500 billion over the coming years — underscores the extent to which securing data center capacity has become a matter of direct national security interest.

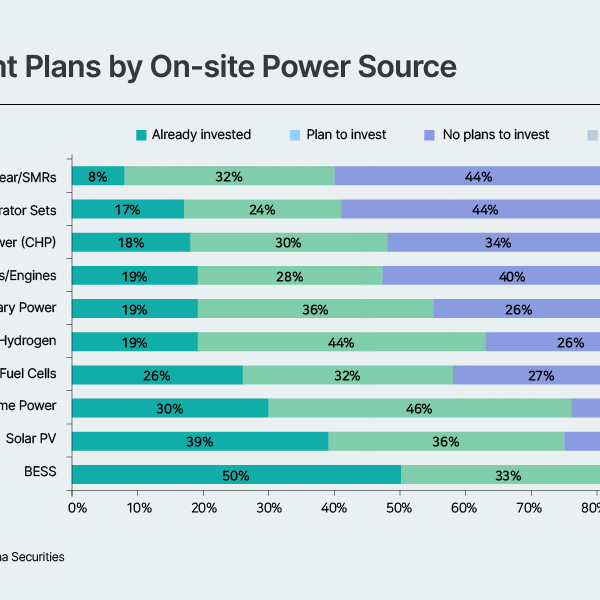

In the era of data center prioritization, the binding constraint is not chips, but electricity. As power-intensive data centers proliferate rapidly, the share of U.S. electricity demand attributable to data centers is projected to rise from 1.9% in 2018 to as much as 12% by 2028. In Europe, overall electricity demand declined at an average annual rate of 0.5% over the past 13 years. However, with the expansion of data centers, electricity demand is now expected to increase at an average annual rate of 1.5 to 2.1% over the next six years. As strategic competition has taken concrete form in the race to build AI data centers, the focus on data has, in turn, been translated into a focus on securing electricity. This is where batteries come into play. The first reason batteries are relevant relates to the power grid. While the construction of a data center itself can be completed within two to three years, building power infrastructure and securing grid connections can take as long as seven to eleven years. Increasingly long wait times for grid interconnection have become a significant burden for data center operators, who have begun investing in on-site generation facilities in order to reduce the amount of time required to secure power supply. In most cases, the preferred generation sources are solar power and LNG-based gas turbines, both of which have relatively short construction timelines. Solar power, however, is constrained by limited hours available for power generation. To compensate for this inherent intermittency, energy storage systems (ESS) are paired with solar installations. On the other hand, LNG-based gas turbines do not inherently require energy storage, but given the nature of on-site power generation, real-time mismatches between electricity supply and demand are unavoidable.1 To manage these imbalances, the installation of battery energy storage systems (BESS) is expected to increase. According to a survey of on-site power generation operators conducted by Alphastruxure and Hana Securities, 50% of respondents reported that they have already begun investing in BESS, while 33% indicated plans to do so. Because BESS can be applied to generation sources beyond solar power such as LNG and small modular reactors (SMRs), it has emerged as the most broadly adopted solution.

1 Data center electricity consumption fluctuates continuously, while power plants face limitations in adjusting output instantaneously in response to demand.

The second pillar of BESS demand growth as it relates to data centers is the increase in power demand. In October 2025, NVIDIA presented a new roadmap for building a data center power ecosystem at the Open Compute Project (OCP) Summit. According to the roadmap, as the company’s GPU architectures transition from Hopper to Blackwell, power consumption per AI server rack has risen from the tens of kilowatts to the hundreds of kilowatts. Looking ahead, when the Rubin architecture is commercialized in 2026–2027, power demand per rack is projected to reach approximately 1,000 kilowatts (1 MW). Given the power usage characteristics of AI data centers — where thousands of GPUs fluctuate between 30% and 100% utilization on a per-millisecond basis — the commercialization of Rubin-class GPUs is expected to place significant strain on power grids and disrupt the balance of electricity supply and demand. As a result, the installation of ESS for load leveling is expected to increase.

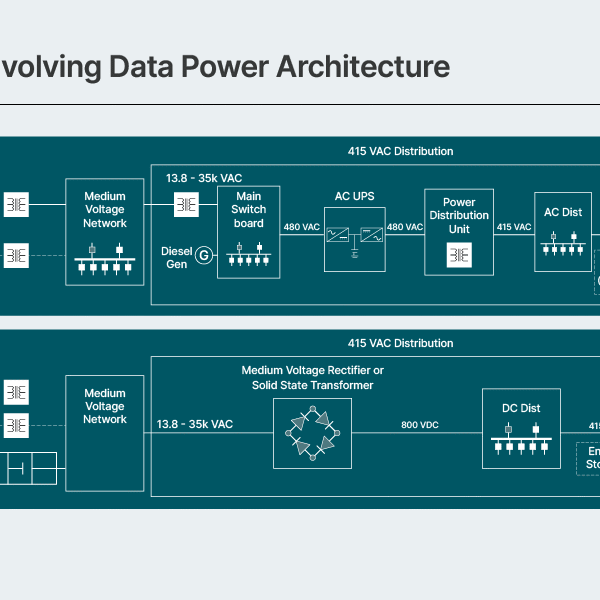

In addition, NVIDIA has outlined a roadmap in which it seeks to minimize power conversion losses by shifting power architectures within data centers from a mixed alternating current (AC)–direct current (DC) configuration to a DC-centric structure. DC is better suited than AC to handle higher voltages while reducing conversion losses, because of the higher operating voltages necessitated by increased overall power consumption. As a result, data centers themselves are evolving into large-scale, DC-based power networks. This shift is expanding the role of BESS, which is an inherently DC-based system. Under the current AC-driven data center model, batteries primarily function as emergency backup power sources. However, as data centers transition toward DC-based power architectures, the role of batteries can expand into that of continuously operating power buffers. As a result, both the penetration rate and installed capacity of BESS within AI data centers are expected to increase.

The Importance of LFP

As the BESS market expands, the importance of lithium iron phosphate (LFP) is also increasing. In electric vehicle batteries, energy density is a critical factor, and ternary cathode chemistries such as nickel-cobalt-manganese (NCM) and nickel-cobalt-aluminum (NCA) are therefore expected to retain their leading position. The BESS market, however, operates under a different set of requirements, because the performance criteria demanded of BESS differ fundamentally from those of electric vehicle batteries.

Electric vehicle batteries are typically charged once every three to four days. In Asia and Europe, where the average annual driving distance for passenger vehicle owners is around 12,000 kilometers, this translates into an average of approximately 0.09 charge–discharge cycles per day, or about 34 cycles per year. In North America, where average annual driving distances exceed 20,000 kilometers, the corresponding figures are roughly 0.17 cycles per day, or about 63 cycles per year. On the other hand, BESS requires far more frequent charge and discharge cycles due to its function. BESS is designed to balance mismatches between electricity supply and demand. Energy is stored during the daytime and discharged at night, while within data centers, BESS systems may cycle multiple times a day to regulate power loads. On average, BESS undergoes approximately 1.3 charge–discharge cycles per day, equivalent to roughly 475 cycles per year, and BESS deployed for load leveling requires even more frequent cycling.

Battery cycle life is determined not by time, but by the number of charge–discharge cycles. As the number of cycles increases, battery degradation accelerates and cycle life declines rapidly. When converting the cycle figures discussed above into a time-based lifespan, electric vehicle batteries can be expected to last at least approximately 9.6 years in North America, and around 18 years in Asia and Europe. BESS, by contrast, is required to undergo more than 400 charge–discharge cycles per year on average, limiting its expected lifespan to roughly 7.6 years at most. In other words, unlike electric vehicles, BESS is charged and discharged repeatedly on a daily basis, leading to faster degradation and a shorter operational life. As a result, ESS applications demand battery structures that provide greater stability and the capability of withstanding a significantly higher number of charge–discharge cycles.

In addition, because electric vehicles are a means of transportation, weight and volume are critical considerations. The battery’s weight must be carried by the vehicle itself, so lighter batteries improve energy efficiency. At the same time, vehicles contain many internal components, limiting the amount of space that batteries can occupy. For these reasons, electric vehicle batteries must deliver high energy density, because it allows more energy to be stored within the same volume or weight.

By contrast, ESS is a stationary system that is installed at a fixed location and does not require mobility. Therefore, battery size and weight have limited impact on overall system performance, even when they are relatively large or heavy. ESS installations can also maximize the use of available space depending on site-specific conditions, such as factories, power grids, and solar power plants. In other words, for ESS, total capacity matters more than energy density. Because energy density is the primary driver of battery cost, ESS can accommodate lower-cost battery chemistries than those used in electric vehicles. This is also a result of ESS applications facing far fewer constraints related to size and weight.

Ultimately, the ESS market is one in which cycle life takes precedence over energy density, and battery chemistries should be designed accordingly to meet these requirements. Achieving long service life requires minimizing battery degradation over time, and, in addition to the amount of charge–discharge cycles, a key variable determining the rate of degradation is oxygen. Transition metals such as nickel, cobalt, manganese, and iron are inherently unstable in their natural state because they lose or gain electrons to achieve stability when bonding with other atoms — most notably oxygen. A more familiar term for this process is “oxidation.”

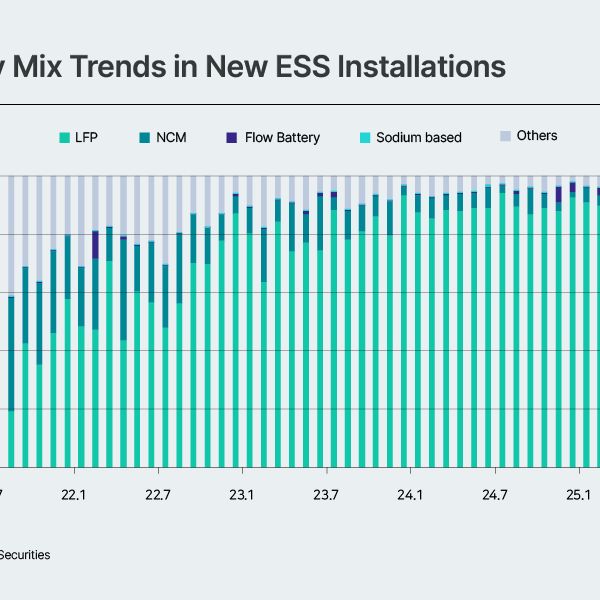

Nickel, cobalt, manganese, and iron are all stabilized by bonding with oxygen. As the number of charge–discharge cycles increases, however, oxygen can be released from these structures, leading to rapid battery deterioration. For this reason, the strength of the bond with oxygen is a key variable in determining battery longevity. LFP, however, offers superior lifetime characteristics compared to the ternary batteries that use transition metals like nickel, cobalt, and manganese because phosphorus, a constituent element of LFP, forms significantly stronger covalent bonds with oxygen. This makes LFP better suited for ESS, despite the ability of ternary cathode chemistries to provide the higher energy density that makes them more advantageous in mobility applications. Reflecting this structural advantage, LFP’s share of the global ESS market has surged from approximately 25% to around 90% over the past four years. In Korea, the ESS market remains relatively small, with ternary batteries still being widely used. Over time, however, the Korean market is expected to follow a trajectory similar to that of the global ESS market.

Opportunities for Korean Companies in the LFP ESS Market

As geopolitical shifts have elevated both data and batteries into security assets, the basis for growth in the ESS market has expanded from decarbonization to national security. As batteries are increasingly treated as strategic assets rather than commodities, the U.S. and European markets are likely to offer expanding opportunities for nations with established battery supply chains. However, few countries beyond Korea and Japan possess meaningful battery supply chain capabilities, and of those two nations, Korean companies have a clear advantage due to the conservative investment stance of Japanese battery manufacturers. Additionally, Korea currently holds the largest share of battery manufacturing facilities in the United States, and as batteries are increasingly treated as security assets, the strategic value of U.S.-based production capacity is expected to become even more pronounced. In terms of battery type, the United States is actively pursuing a reduction its dependence on a Chinese supply of LFP, which has traditionally been a market dominated by companies from China. This effort combines the use of tariffs as a deterrent with incentives included under the Advanced Manufacturing Production Credit (AMPC), such as investment tax credits and production subsidies. As these policy measures take effect, Korean companies are expected to rapidly increase their market share in the U.S. LFP ESS market.

SK On has taken concrete steps in this direction, such as signing an agreement with the U.S.-based renewable energy developer Flatiron Energy Development to supply up to 7.2 GWh of LFP ESS batteries between 2026 and 2030. Under the agreement, SK On will start with the supply of containerized BESS units featuring 1GWh of LFP batteries for a project in Massachusetts, with deliveries beginning in the second half of 2026. At the same time, Korean companies such as LG Energy Solution are also seeing an increase in related ESS orders. The rise in data center–driven ESS demand — rooted in prioritization from the U.S. and China — and the resulting growth in demand for LFP batteries represent a significant opportunity for Korea’s battery industry. And since batteries are emerging as strategic materials in the current geopolitical environment, such battery competitiveness may also serve as a national security asset over the longer term.

※ This column reflects the views of the author and does not necessarily represent the official position of SK Innovation.

■ Related articles

- All-Solid-State Batteries: A Game Changer Shaping the Future of the Electric Vehicle Era

- SK On Unveils Breakthrough in Next-Generation Cathode Research

- SK Innovation, SK On Partner with Standard Energy on Safer ESS

- SK On Opens All-Solid-State Battery Pilot Plant, Eyes 2029 Commercialization

- SK On Expands into U.S. BESS Market with LFP Batteries