As the energy storage system (ESS) market rapidly expands, lithium iron phosphate (LFP) batteries have been gaining significant attention. However, in industries beyond ESS — such as humanoid robots, drones, and electric vehicles — the importance of ternary batteries is becoming increasingly evident.

This article examines the rationale for the continued growth of the ternary battery market from three perspectives: the emergence of new markets such as robotics and drones, the growing importance of battery recycling, and the expansion of the autonomous vehicle market.

Battery Requirements for Robots and Drones

As AI expands into the physical world, the most profound transformations are occurring in the means of production and transportation. The era of so-called “physical AI” is taking shape as robots increasingly replace human labor in production, while urban air mobility (UAM), drones, and autonomous vehicles redefine mobility. At the core of this shift lies the battery — the “stamina” that powers robots and drones. The challenge, however, is that these emerging devices demand performance characteristics fundamentally different from those required by electric vehicles or ESS. These distinct requirements ultimately reinforce the case for the continued growth of ternary batteries.

One key factor behind the rapid rise of LFP batteries in the electric vehicle market is the adoption of Cell-to-Pack (CTP) technology. CTP refers to a design approach that eliminates the intermediate module stage by integrating cells directly into the battery pack. This architecture allows LFP batteries to compensate for their relatively lower cell-level energy density by improving efficiency at the pack level.

The feasibility of CTP largely stems from the high thermal stability of LFP chemistry. Because LFP cells carry a lower risk of explosion under overcharging or external impact, protective structures between cells can be simplified. This enables manufacturers to reduce safety components within the pack and utilize the freed space to add more cells. As a result, LFP packs using CTP technology can achieve a volumetric cell-to-pack ratio (VCTP) of around 80%.

By contrast, ternary batteries require more complex cooling and protective structures between cells due to the risk of thermal runaway. Consequently, their pack-level space utilization typically remains around 60%. In effect, while LFP batteries have historically lagged behind ternary batteries in cell-level energy density, the adoption of CTP has allowed them to close the gap at the pack level. This shift has contributed to LFP’s growing market share in the electric vehicle segment.

The situation differs, however, in robotics and drone applications. Humanoid robots and drones have limited space to accommodate large battery packs, and increases in pack weight are difficult to tolerate. Both volume and weight directly affect flight capability and mobility. In these emerging markets, improvements in pack-level space efficiency through structural optimization are less important than enhancing the intrinsic energy density of individual cells. As a result, batteries for robots and drones must compete primarily at the cell level rather than the pack level.

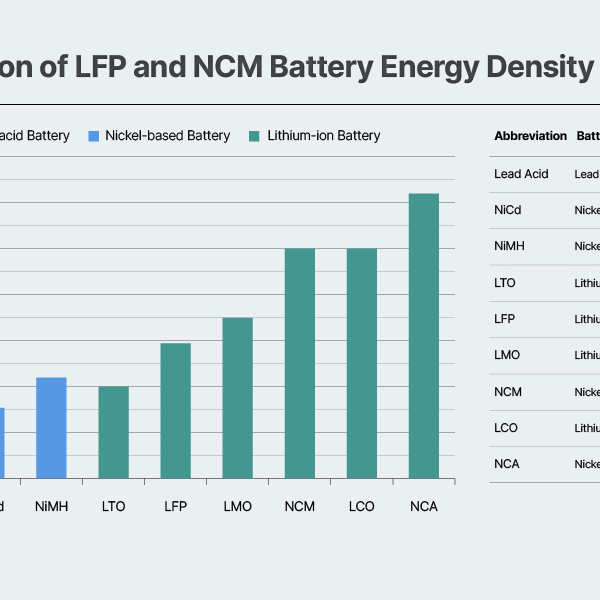

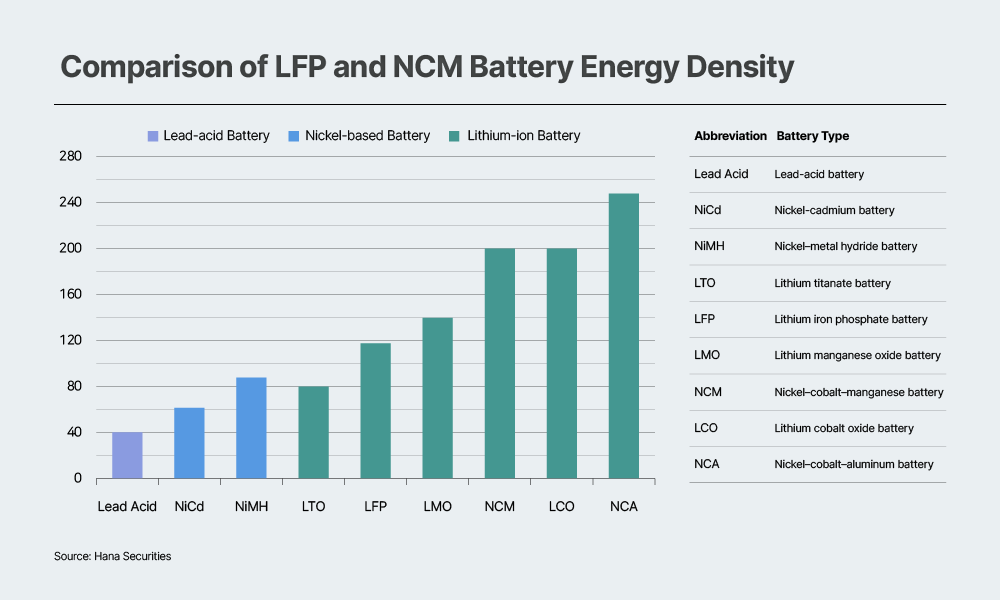

A comparison of major battery chemistries based on cell-level gravimetric energy density (Wh/kg) shows that ternary batteries maintain a clear advantage over LFP. On average, LFP cells deliver around 90–170Wh/kg, while ternary batteries typically reach 200–300Wh/kg.

Recent announcements from Chinese manufacturers indicate that the energy density of mass-produced LFP batteries has improved to as high as 186Wh/kg. Additionally, Contemporary Amperex Technology Co., Limited (CATL) has set an energy density target that exceeds 200Wh/kg through its fourth- and fifth-generation LFP products. Despite these advances, however, LFP still faces inherent limitations. Its lower average operating voltage (3.2V for LFP versus the 3.6–3.8V achieved by nickel-cobalt-manganese (NCM)) and relatively limited theoretical capacity make it difficult to significantly narrow the cell-level energy density gap with ternary chemistries.

Even if fifth-generation LFP products reach cell-level gravimetric energy densities around 210Wh/kg, a gap of roughly 25% would remain compared to commercial nickel-cobalt-aluminum (NCA) batteries, which typically achieve around 270Wh/kg. Moreover, if silicon anodes become widely commercialized in the future, ternary batteries — whose higher operating voltage allows for greater gains in cell-level energy density — are likely to see greater performance improvements than LFP. This dynamic could further widen the gap between the two chemistries.

Of course, ternary batteries face their own challenges. As energy density increases, structural instability in the crystal lattice can emerge. However, the prospects for addressing this issue have significantly improved recently as a result of advances in single-crystal cathode technology.

Most ternary cathode materials currently in use feature a polycrystalline structure. In polycrystalline cathodes, multiple small particles form a composite structure that can develop microcracks during repeated charge-discharge cycles. By contrast, single-crystal cathodes consist of a single, larger crystal structure, which reduces crack formation and enhances cycle stability. This characteristic is particularly advantageous under high-voltage and high-energy density operating conditions.

In fact, several battery industry players, including cathode material manufacturers, have recently reported progress in commercializing single-crystal NCM materials and improving high-voltage stability. These developments are expected to further strengthen the cell-level competitiveness of ternary batteries in the future.

One such company is SK On, which announced in January that it has successfully developed a high-nickel single-crystal cathode material through joint research with Seoul National University. The material features particles approximately 10μm in size — about twice the size of conventional cathode particles. With a nickel content exceeding 94%, the material is classified as an “ultra-high-nickel” cathode. Through particle-level single crystallization, the material is expected to improve stability while enabling longer driving ranges on a single charge in electric vehicles.

Meanwhile, high power capability is another critical consideration. In batteries, “power” refers to the rate at which energy can be discharged over time, and is typically expressed as the C-rate. A rate of 1C means that the battery’s full capacity is discharged within one hour. When a drone takes off or a robot climbs stairs, the battery may require high-rate discharge in the range of 3–10C. This represents a significantly more demanding set of conditions than the 0.5–1C typically required while driving automobiles at steady speeds.

Ternary batteries offer advantages over LFP in terms of electrical conductivity and lithium-ion diffusion rates. In particular, higher nickel content tends to support stronger high-power performance. In markets such as robotics and drones — which require simultaneously high energy density and high power output — the strengths of ternary batteries are likely to become even more pronounced.

The Growing Importance of Battery Recycling

The emergence of the battery recycling market is another key factor reinforcing the value of ternary batteries. The need for recycling is not driven solely by environmental considerations, but is more fundamentally a matter of supply chain security. Today, one of the most significant risks facing the battery industries in the United States and Europe is their growing dependence on China’s supply chain.

If the battery market continues to expand while remaining reliant on China for the upstream supply of critical minerals — which account for more than half of battery manufacturing costs — the United States and Europe could face considerable vulnerability from an energy security perspective.

Battery recycling offers a viable pathway in the face of these supply chain considerations. In the era of internal combustion engine vehicles, petroleum — the primary energy source — was irreversibly converted into carbon dioxide during combustion. By contrast, key minerals such as nickel, cobalt, manganese, and lithium, which serve as the energy carriers in the electric vehicle era, remain intact even after a battery reaches the end of its service life. As a result, recovering and reusing these minerals from spent batteries can help address the supply chain considerations described above.

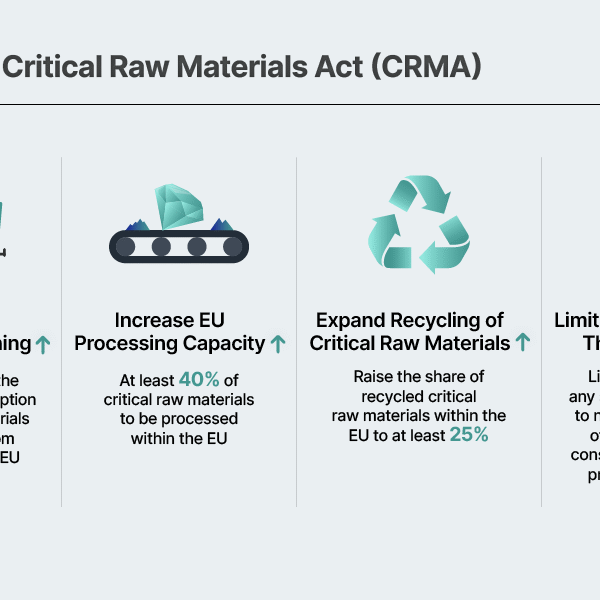

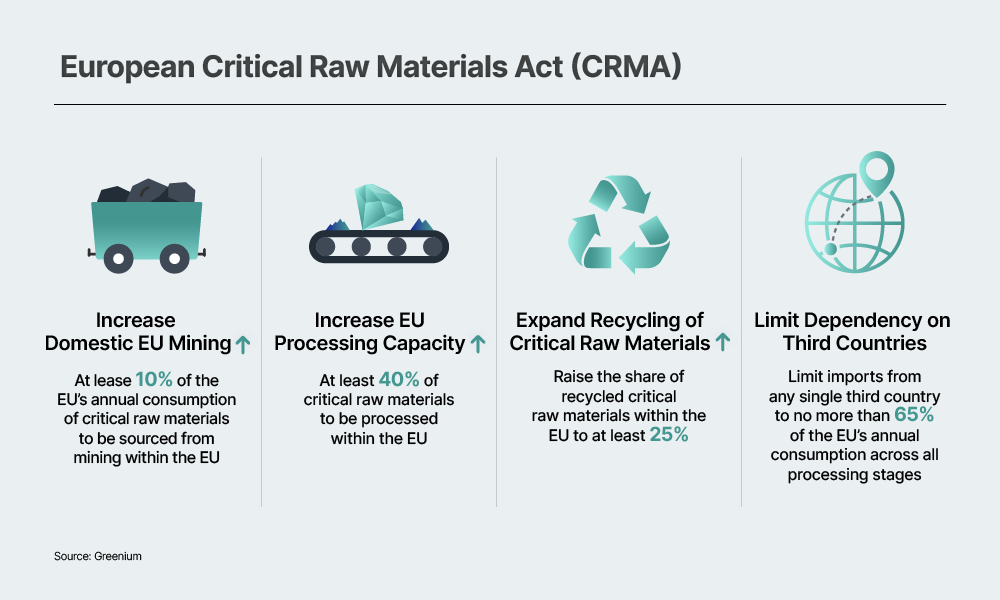

The United States and Europe are gradually moving to institutionalize recycling as a prerequisite for participation in the battery market. A representative example is the European Union’s Critical Raw Materials Act (CRMA) and the EU Battery Regulation (EUBR). The CRMA aims to increase the share of domestically recycled raw materials to 25%, while the EUBR requires that, from 2031 onward, at least 16% of cobalt, 6% of lithium, and 6% of nickel used in batteries come from recycled sources. The United States is also expected to tighten recycling-related regulations over the long term. In this policy environment, the fact that ternary batteries offer stronger recycling economics than LFP batteries carries significant implications.

The economic viability of battery recycling is largely determined by the market value of recoverable metals. This is where the gap between LFP and ternary batteries becomes particularly evident. Ternary chemistries — such as NCM and NCA — contain metals with relatively high market value. As a result, direct recycling can generate expected profits of roughly $10–$22 per kWh.

By contrast, the iron and phosphate contained in LFP batteries have relatively low market value, which significantly reduces profitability when conventional hydrometallurgical or pyrometallurgical recycling processes are applied. Even when direct recycling technologies are used, profits tend to be minimal and, depending on the scenario, losses may occur (Nature Communications, 2024). To elaborate on this, a 2025 study published in PMC indicates that an LFP-dominant scenario (CC-LFP) could result in cumulative losses of approximately $3 billion by 2060. From a long-term perspective, it may therefore be difficult for LFP batteries to achieve strong recycling economics.

As recycling requirements become institutionalized, the cost gap between LFP and ternary batteries is expected to gradually narrow. Currently, the price difference between LFP and ternary cathode materials is estimated to be about 25%. However, revenues generated from NCM recycling could offset a portion of cathode material costs, potentially reducing the effective cost gap to around 10%. Because LFP recycling tends to incur additional costs rather than generate meaningful value, the cost gap may narrow even further. Over the long term, recycling could effectively function as a “gate fee” for market entry, which may weaken the competitiveness of LFP batteries.

ESS, however, represents an exception. In ESS applications, LFP’s long cycle life and cost advantages remain decisive, and policymakers may be more inclined to relax recycling requirements or provide cost support specifically for ESS deployments. The situation is different for batteries used in electric vehicles, robots, and drones, however. As recycling requirements become progressively stricter, the structural advantages of ternary batteries are likely to become increasingly pronounced in these markets.

The Expansion of the Autonomous Vehicle Market

The future of the automotive industry lies in autonomous driving. With the history of technological progress having been largely a process of maximizing the value of time, the commercialization of autonomous driving, which maximizes the driver’s time — one of the few remaining forms of untapped time value — can be seen as an inevitable step in that trajectory. Autonomous driving also drives a sharp increase in in-vehicle computing demand, which in turn directly leads to higher battery energy consumption.

At present, Level 2 autonomous driving systems typically consume around 200–600W of power. Waymo’s Level 4 autonomous driving system consumes approximately 1kW. Early versions of GM Cruise’s autonomous driving system require around 3–4kW, though the company aims to reduce this to roughly 1kW in next-generation systems (Energy Central). Meanwhile, the thermal design power (TDP) of NVIDIA’s AGX Orin SoC-based computing platform is about 800W.

If a 1-kW autonomous driving system operates continuously throughout the day, the available driving range of an electric vehicle can decrease by an average of 10–30%. In urban driving conditions in particular, the reduction in driving range can reach as high as 30%. In practical terms, this means that an electric vehicle equipped with a 70-kWh battery pack may consume roughly 7–21kWh of its battery capacity to support autonomous driving computations.

In this context, the energy density gap between LFP and ternary batteries once again becomes a critical factor. If a Level 4 autonomous vehicle were to use an LFP battery pack to achieve the same driving range, it would need to carry a heavier battery pack than one using NCM batteries. The resulting increase in pack weight could lead to higher overall energy consumption, creating a negative feedback loop. As computing demand in autonomous vehicles continues to grow, the competitive advantages of ternary batteries are therefore likely to become even more pronounced.

The Challenge: Reducing Costs

Despite their advantages in energy density, ternary batteries still lag behind LFP in terms of price competitiveness. According to data from S&P Global, LFP cells are priced at around $60 per kWh — more than 25% lower than NCM cells, which cost approximately $80 per kWh. Unless this cost gap is narrowed, the technological advantages of ternary batteries may not be fully realized.

Recently, dry electrode technology has emerged as a key innovation for reducing battery manufacturing costs. In wet process electrode production, the cathode materials are dissolved in a solvent to form a slurry, which is then coated onto an aluminum current collector and passed through a long drying oven. This conventional process represents the single largest cost component in cell manufacturing. It also requires solvent recovery and treatment systems because it uses N-methyl-2-pyrrolidone (NMP), a hazardous solvent.

Dry electrode technology takes a different approach. Instead of using solvents, cathode powder and binder materials are directly formed into a film and pressed onto the current collector. Because this process eliminates the need for drying ovens and solvent recovery systems, it can significantly reduce capital expenditures (capex) and energy costs in battery cell factories.

Tesla began mass-producing a portion of its 4680 cells using dry electrode technology in late 2024. SK On is likewise expanding its investment in research and development related to dry electrode technology in an effort to strengthen its price competitiveness.

If dry electrode technology reaches full commercialization, the manufacturing cost gap between ternary batteries and LFP could narrow to within roughly 10%. In that case, the expansion of ternary batteries — already advantaged in energy density, power performance, and recycling economics — could accelerate further in emerging markets such as robotics, drones, and autonomous vehicles.

Strengthening Ternary Battery Competitiveness Through Localized Production

The battery market is likely to evolve into an environment in which demand from different downstream applications leads to LFP and ternary batteries growing alongside each other. As discussed earlier, LFP is likely to solidify its leadership in the ESS market, where long lifespan and charge-discharge cycle stability are critical factors. In contrast, ternary batteries are expected to secure a leading position in the robotics and drone markets, and over the long term, the autonomous vehicle sector is also likely to maintain a market structure centered on ternary chemistries.

Policy trends in the United States and Europe that emphasize battery recycling are also creating a favorable environment for ternary batteries. At the same time, both regions are increasingly prioritizing domestic battery production, a shift that is expected to expand opportunities for Korean companies.

Despite short-term market headwinds, SK On is continuing to prepare for future demand by mass-producing ternary batteries at SK Battery America in Georgia and preparing to launch mass production of ternary batteries at its joint venture plant with Hyundai Motor Group. Given the strong competitiveness that Korean companies have established in the ternary battery segment, opportunities in related markets are likely to expand further in the years ahead.

※ This column reflects the views of the author and does not necessarily represent the official position of SK Innovation.

■ Related articles

- [Expert Lens] How Energy Security Presents a New Opportunity for the Korean Battery Industry

- [INTERBATTERY 2026 Preview] Unlock the Next Energy – Next-Generation Battery Innovation at the SK On Booth

- [Sustainable Power] SK On Makes Great Batteries — and Sustainable Progress

- All-Solid-State Batteries: A Game Changer Shaping the Future of the Electric Vehicle Era

- SK On Unveils Breakthrough in Next-Generation Cathode Research